- Banks are sitting down to 2H 2020 hungry for assets but are required to order from a limited and mostly unappetizing menu.

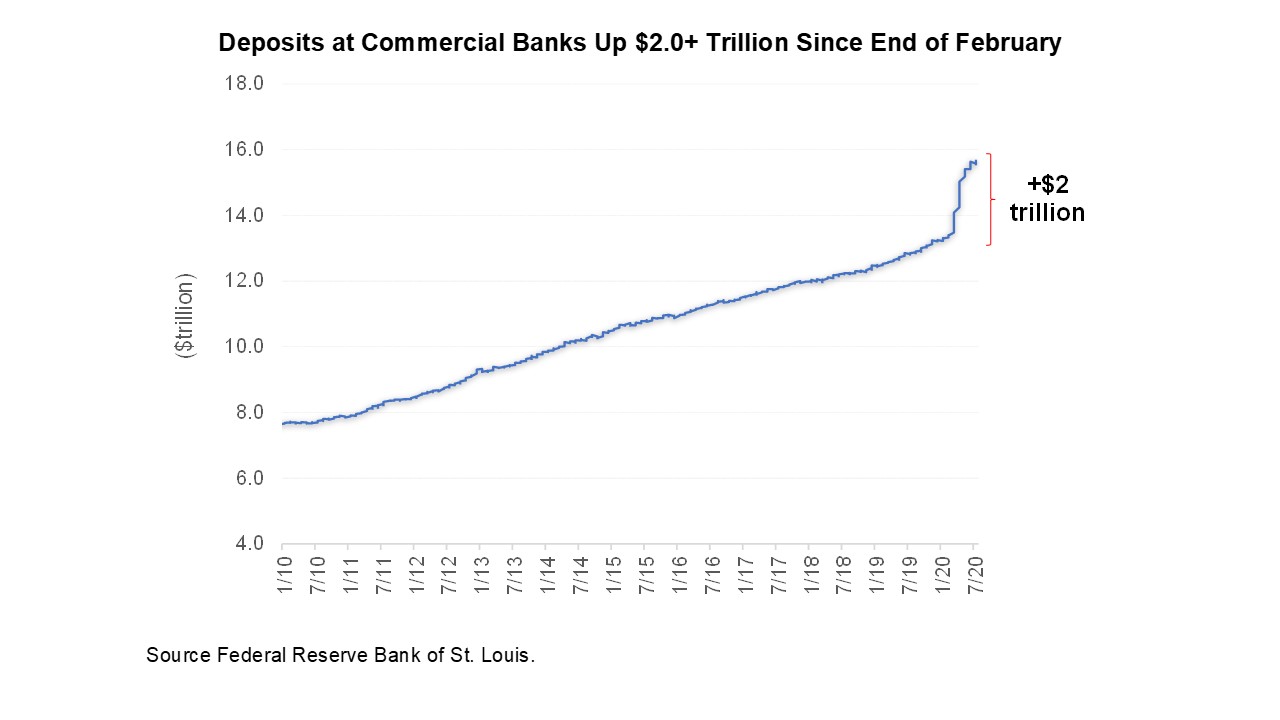

- COVID stimulus programs have translated into the greatest buildup in bank deposits in U.S. history.

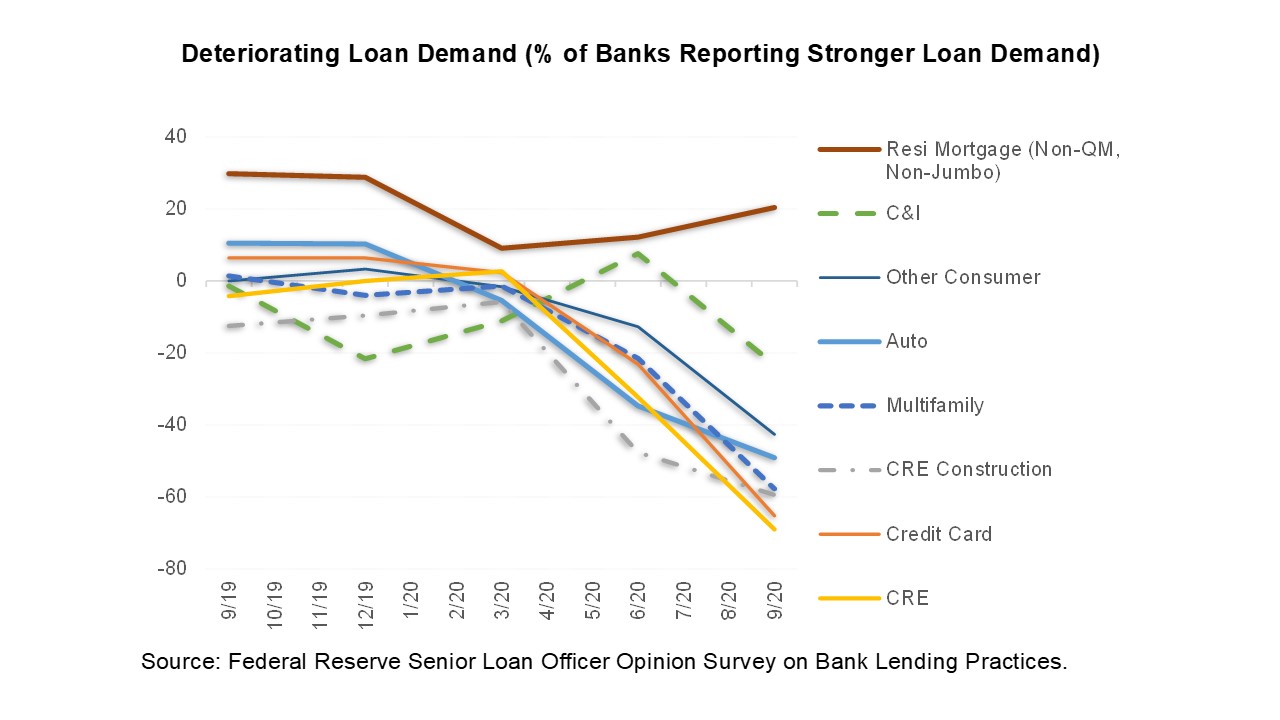

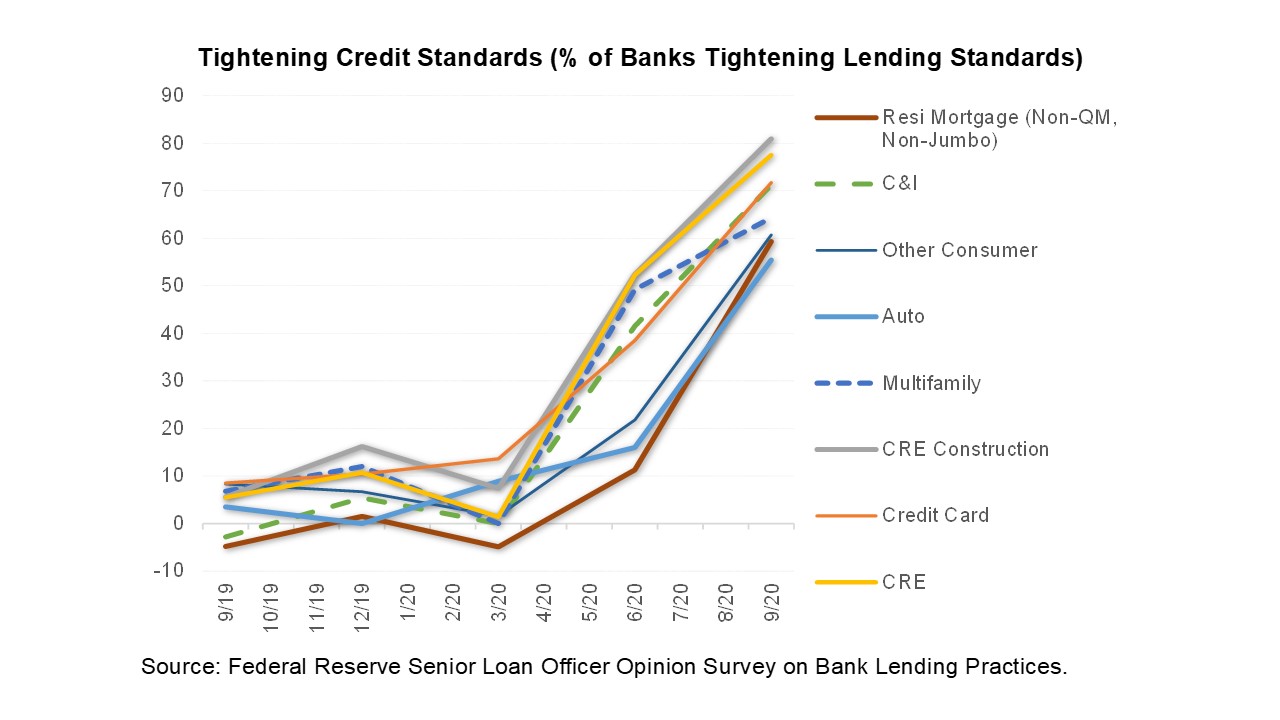

- While banks are awash in low-cost funding, attractive income-earning assets have proved elusive because loan demand has collapsed and credit standards have constricted.

- For lenders, fund finance is uniquely positioned compared to the evolving credit risks in business, consumer and CRE loan portfolios.

- While fundraising slowed in 1H 2020, LPs, on net, reported expectations for increased allocations to alternatives in the long term after COVID, according to a Preqin survey.

- This is intuitive, because the same formula that has supported a rotation into private capital in recent years is still in full effect: yields are historically low, valuations are historically high, and liability-matched investors are reporting disappointing realized returns.

- Added to this, cross-asset correlations in public markets pose a real challenge for portfolio managers, as markets from equities to high yield have moved up in sync to date in 2020. The search for uncorrelated returns favors increased allocations to private funds.

- In 2H 2020, LPs may sense a limited window within which to acquire discounted assets. The perceived opportunity is on the private side.

- Our LPA review experience shows, even with the slowdown in fundraising in 1H, lenders found plenty of prospects to pursue.

- From a fund perspective, the cost-of-funds advantage from a LIBOR-indexed subscription facility and the operational efficiencies (e.g., speed to execution) are indispensable in the current investment environment.

Bank Deposits Have Soared But Attractive Assets Are Scarce

U.S. banks have experienced an unprecedented influx of deposits since the onset of COVID. Stimulus programs explain the increase, as does the preference by companies and individuals to hold cash during uncertain times. Total deposits at commercial banks are up more than $2 trillion since the end of February, and, in April alone, deposits grew at a 74% annualized rate. Banks responded immediately to this abundance of low-cost funding by expanding holdings of Treasuries and MBS – the most readily scalable assets. These assets, however, earn paltry returns, even in the context of the Primary Dealer Credit Facility and the reduced discount window rate. Depository institutions are graded on net interest margin, which means that over time, pressure will mount to deploy balance sheets into income-earning assets. Bank engagement in fund finance originations should continue to be high, consistent with the first half of the year.

While banks are flush with deposits, loan origination is proving challenging, in part because loan demand has collapsed (with the exception of demand for residential mortgages where refi burnout will eventually come into play). At the same time, credit standards have ratcheted tighter across the board. Borrowers are now more scarce and the credit approval hurdle higher. We see this dynamic as favoring fund finance origination where fundraising is providing a steady stream of borrowers and credit conditions have been far less eventful than in business, consumer and CRE loan portfolios.

Persistently Low Rates, High Valuations and Public Market Cross-Asset Correlations to Support Further Private Market Capital Inflows

Private market fundraising slowed in the first half of the year, with the number of funds closed down 40% in Q2 compared to the prior-year period, according to Preqin data. Worldwide, 861 funds closed in the first half, raising $443 billion in capital. LPs decreased the number and size of commitments as COVID rippled through markets. That’s not the whole story, however. Nearly a third of LPs expect increased exposure to alternatives in the long term following COVID, and an even higher share of fund managers expect a long-term positive impact on the alternatives industry. The same formula that pushed private market assets under management to a record $7.2 trillion in 2019 remains in full effect in 2020.

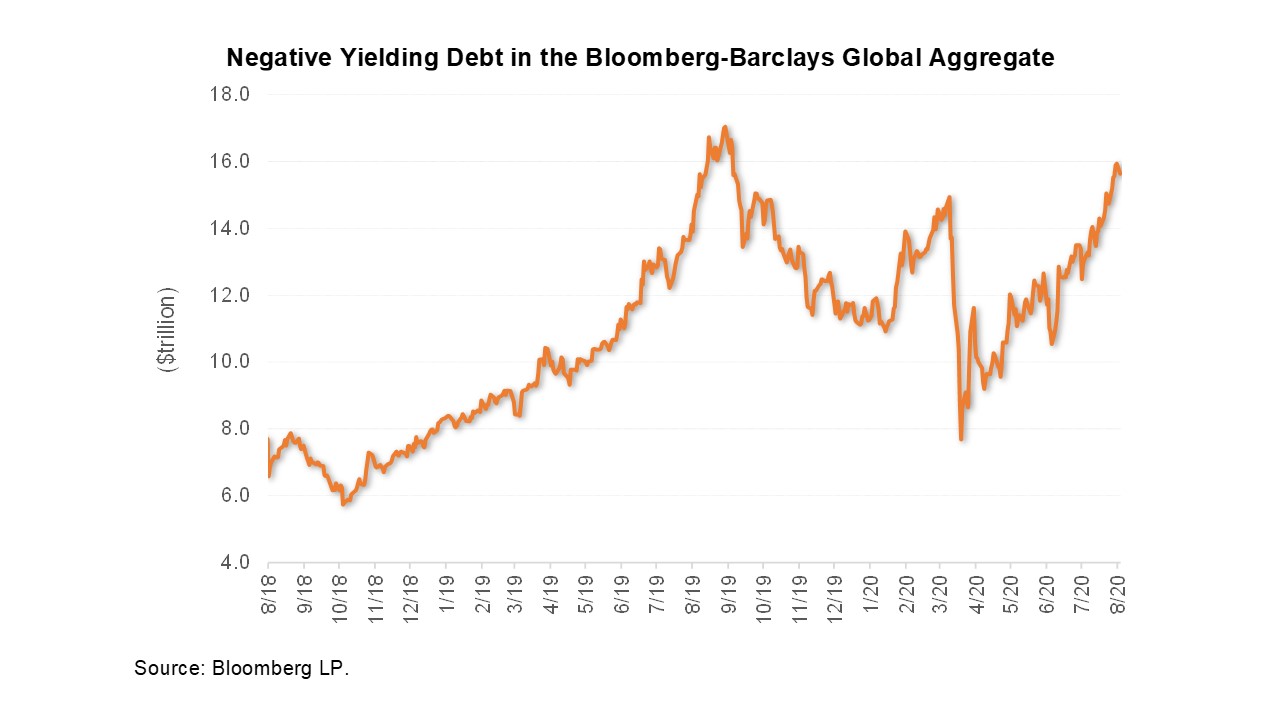

That formula includes low real returns, soaring public market valuations, and disappointing realized investment performance for liability-matched investors. At the end of July, the global supply of negative yielding debt in the Bloomberg-Barclays Global Aggregate Index sat just shy of $16 trillion. Pension funds, insurance companies and other liability-matched investors are hard-pressed to replace investment portfolio income that historically came from the fixed income portfolio. For the first half of 2020, U.S. institutional pension plans posted a mediocre median return of 3.36%, according to Wilshire Associates. Larger plans with greater allocations to alternative investments fared better than small plans. On the whole, liability-matched investors are likely to turn further to private funds as the spread between the 8% preferred return offered in the typical private fund has never been higher compared to the ten-year Treasury yield than in 2020.

This Outlook is Consistent with Our 1H Experience

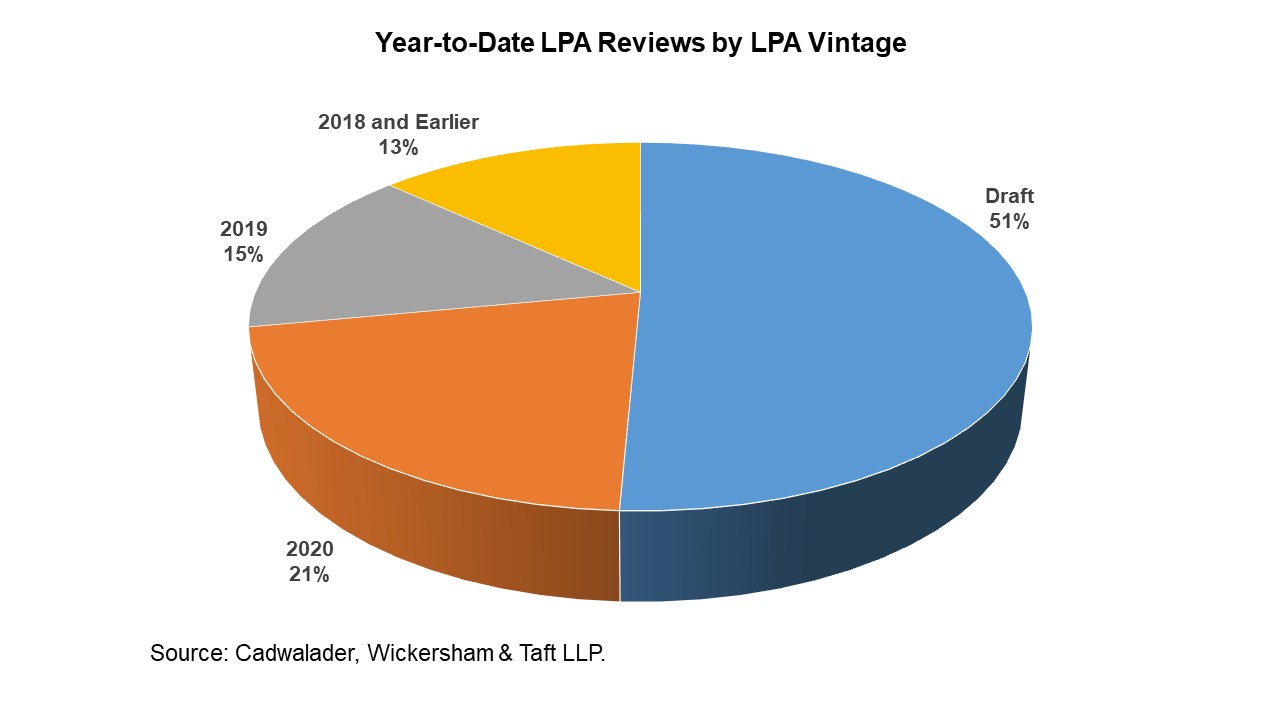

As Mike Mascia and Wes Misson reported last week, our deal volume in the first half handily exceeded the prior year. While fund formation slowed, lenders have been able to find ample opportunities. Of the LPAs we’ve reviewed year to date, nearly three-quarters were from funds closed or slated to close in 2020. The slowdown in fund formation so far hasn’t been a significant encumbrance to fund lending.

Conclusion

The same wave of macro drivers that the fund finance market has been riding is carrying over into 2H 2020. Added to this, banks have a flood of deposits to digest – additional rounds of stimulus could add more – while originations in other bank loan categories may be challenged. Together, these all point to an outlook for strong origination volume in the remainder of the year (and, with that, a competitive market between lenders). For funds, the cost advantage and operational efficiency from a credit facility are now as important as ever.