Why is this topic suddenly of interest?

Irish Investment Limited Partnerships (“ILPs”) have been around since the introduction of the Investment Limited Partnership Act in 1994 (the “1994 Act”). Due to certain requirements imposed under the 1994 Act, they have seldom been used – there were only six in existence as of January 2021 based upon statistics published by the Central Bank of Ireland (“CBI”).

However, the 1994 Act has now been revitalised by virtue of the Investment Limited Partnerships (Amendment) Act 2020 (the “2020 Act”) to make it fit for modern-day investment purposes and comparable to other fund domiciles. Marking the signing of the Statutory Instrument, the Irish Minister of State at the Department of Finance, said: “The changes will further support Ireland’s offering as a top-tier global location of choice for financial services investments.”

In addition to the 2020 Act, the CBI has also helpfully updated its Alternative Investment Fund (“AIF”) Rulebook for closed-ended qualifying investor AIFs (“QIAIFs”) investing in private equity and other illiquid assets, providing clarity in the context of customary features for closed-ended funds, such as capital drawdowns, carried interest, distribution waterfalls and catch-up payments, which are now confirmed as generally permitted for QIAIFs.

The ILP is now expected to become the fund structure of choice for many international fund sponsors, particularly those in the private equity and real asset sectors. As you will see below, as there are generally no leverage restrictions, the ILP can be a useful component of various structures, with a number of options as to subsidiaries and, accordingly, master/feeder fund arrangements. Much like the highly successful Irish Collective Asset-management Vehicle (“ICAV”) that was introduced in 2015, the ILP can be deployed in a number of different types of financing, including NAV or subscription line facilities. We expect that fund finance lenders will begin to see more ILPs appear in borrower groups in the not-too-distant future.

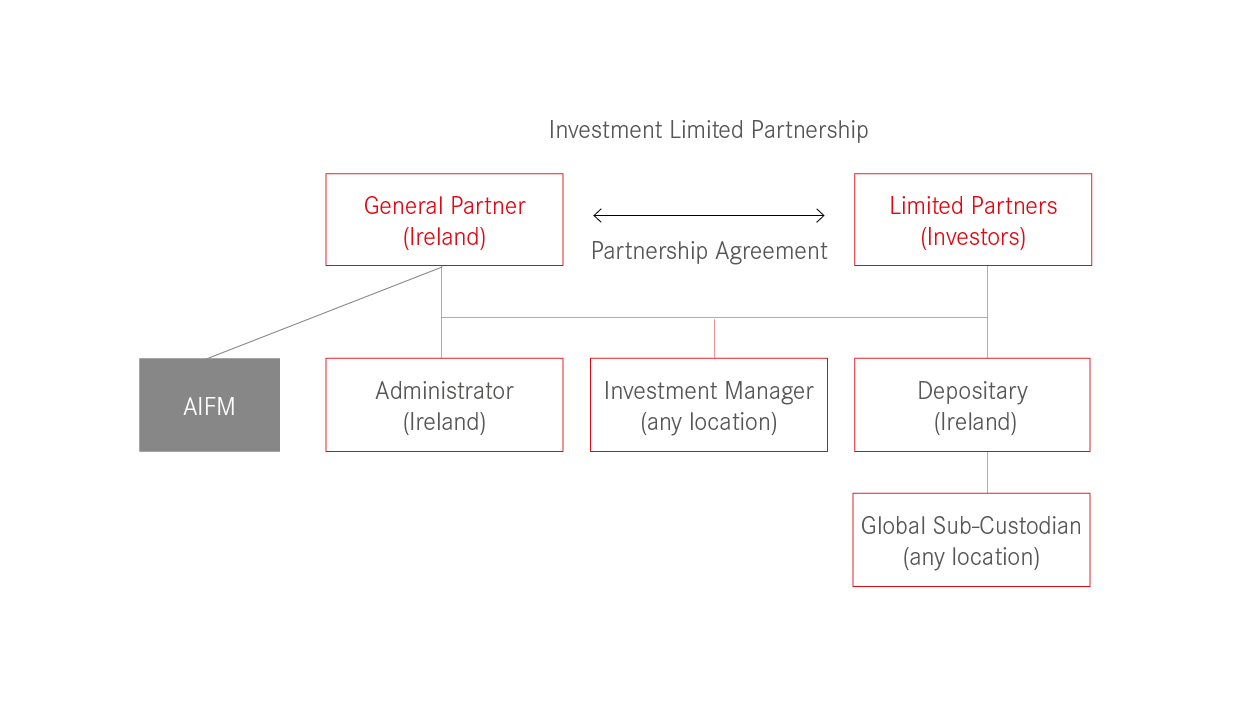

What is an ILP?

An ILP is a partnership that has limited liability for the investors who invest as limited partners (“LPs”). An ILP is not an incorporated entity, so the assets, liabilities and profits belong to the partners in the ILP in accordance with the terms of the limited partnership agreement (the “LPA”), the written document establishing and governing the ILP. As a result, an ILP has no separate legal personality and is treated as tax transparent from an Irish tax perspective.

From an Irish regulatory perspective, an ILP is an AIF which is authorised as a QIAIF. An ILP must be authorised by the CBI and can benefit from the CBI’s 24-hour approval process. There are no material investment restrictions or diversification requirements and no borrowing or leverage limits imposed upon ILPs (unless the ILP is engaged in loan origination). In addition, an ILP may be open-ended, have limited liquidity or be closed-ended.

An ILP must have at least one general partner (“GP”) which has responsibility for managing the business of the ILP and can be held liable for the debts and obligations of the ILP. An ILP may have one or more LPs. There is no limit on the number of LPs permitted in an ILP. QIAIF ILPs are open to professional or well-informed LPs who: (i) are MiFID “professional clients”; (ii) self-certify in writing as being informed investors; or (iii) are appraised by an EU-regulated institution as having an appropriate level of expertise, knowledge and experience. LPs have the benefit of limited liability up to contributed capital (and any outstanding commitments) and the benefit of an extensive and modernised non-exhaustive whitelist of permitted activities which will not cause forfeiture of that liability protection.

The amendments set out in the 2020 Act include the following:

- Umbrella Limited Partnerships. Providing for the establishment of ILPs as umbrella funds with multiple sub-funds and segregated liability between those sub-funds. The ability to establish an umbrella structure, which is already permitted for other types of Irish fund vehicles, will allow managers to establish multiple sub-funds within the same ILP, allowing for separate investors, separate pools of assets and differing investment strategies without the need for multiple ILPs.

- LPA Amendments. Streamlining the manner in which changes may be made to the LPA.

- Safe Harbours for Limited Partners. Expanding the “whitelist” of activities in which a LP can engage without being deemed to be taking part in the conduct of the business of the ILP. This is a welcome clarification for ILPs in terms of the scope of LP activities which can be undertaken without risk of losing the benefit of limited liability.

- Return of Capital. Simplifying the procedures in respect of the return of capital to LPs.

- Redomiciliation. Permitting the redomiciliation of partnerships from other jurisdictions (such jurisdictions to be specified by ministerial order) and setting out a streamlined process for such redomiciliation. The ability to redomicile funds from offshore jurisdictions was introduced in Irish legislation given the increasing preference among investors for regulated onshore jurisdictions. A redomiciled partnership will be authorised by the CBI as an ILP by way of continuation and may continue to use its track record, and the legislation provides that redomiciliation will not operate so as to impact on any agreement entered into by the partnership prior to redomiciliation.

Comment

The introduction of these reforms to the ILP is a welcome and significant development for the Irish funds industry and reflects an industry which is constantly seeking to develop and grow, building on the positive experiences of the many sponsors who have already established funds in Ireland. The enhanced and rebooted ILP 2.0 will further strengthen Ireland’s fund product range, providing an attractive vehicle for promoters seeking to establish private equity, venture capital and “real economy” investment funds in Europe.

Over the past few years, we have seen the ICAV form part of the onshore portion of fund structures (parallel funds, master/feeder fund structures, etc.) and whilst this is likely to continue, as a partnership is the vehicle of choice for many sponsors and investors, it is anticipated that the ILP will soon emerge in such fund structures.

This will be of great interest to sponsors who require offshore and onshore coverage/investment opportunities. As we have seen a surge in the provision of debt finance to ICAVs in such structures, it is also anticipated that fund financing (e.g., subscription line or NAV facilities) to analogous structures containing ILPs will become very common. In most respects, similar key legal, regulatory, tax and practical considerations will arise when advising a lender or borrower on financing arrangements that include an ILP. The typical credit support package (and use of cascading pledges where necessary) is likely to be a common feature where structures include an ILP and the due diligence will also be comparable (although with the extra addition of reviewing the LPA).